TANZANIA: Scirocco Energy Divest its Interest in the Ruvuma Asset

Ruvuma Transaction Highlights

- Total consideration of up to US$16 million comprised of:

- Initial consideration of US$3 million payable on completion of the Proposed Transaction;

- US$3 million payable upon final investment decision being taken by the parties to the Ruvuma Asset Production Sharing Agreement or the JOA as the case may be;

- Deferred consideration of up to US$8 million payable in the form of a 25% net revenue share from the point when Ruvuma commences delivery of gas to the gas buyer;

- Contingent consideration of US$2 million payable on gross production reaching a level equal to or greater than 50Bcf.

- Wentworth to provide Scirocco with a loan of up to $6,250,000 to meet all cash calls pursuant to the Ruvuma JOA arising between the Economic Date of 1 January 2022 and expected Completion timeline.

- The first $3m to be drawn under the loan is interest free however any amounts drawn in excess of $3m will incur interest at a rate of 7% per annum until such time as the grant of the security in respect of the loan is approved by the Minister for Energy in Tanzania.

- The total consideration represents over 200% premium to Scirocco’s current market capitalisation.

- The deal strengthens Scirocco’s balance sheet and, critically, removes the imminent need to raise capital to fund the Ruvuma work programme.

- Completion of the Proposed Transaction follows a formal sales process for the asset and enables Scirocco to accelerate its strategy of building a portfolio of cash generative assets within the sustainable energy and circular economy sectors.

- Those Directors who hold shares, representing 3.2% of the Company’s issued share capital, believe the Proposed Transaction to be in the best interests of the Company and will be voting in favour at the General Meeting.

- In addition the Company has received letters of support for the Proposed Transaction from significant shareholders representing 11.1% of the Company’s issued share capital which confirm that it is their current intention to vote in favour of the resolution at the General Meeting

In line with the requirements of Schedule Four of the AIM Rules, the Company notes that it recorded its interest in the Ruvuma asset at a gross asset value of £14.63 million per its unaudited accounts for the 6 month period ended 30 June 2021. For the audited year ended 31 December 2020, the Company incurred losses relating to Ruvuma asset of £0.81 million.

Capitalised terms are as per the definitions section at the end of the announcement.

Commenting on the Proposed Transaction, Tom Reynolds, Scirocco’s CEO stated:

‘This is a transformative deal that follows lengthy engagement with Wentworth and a two-year sales review process. The deal enables Scirocco to crystallise firm value from this asset which can be deployed into compelling opportunities in line with the Company’s strategy to focus on opportunities within sustainable energy and the circular economy. The deal is appropriately structured to reflect the risk profile of the asset and ensures Scirocco retains value exposure to the ongoing success of the project as it reaches various milestones. Critically, it also provides the Company with the funding to meet the imminent cash calls associated with the work programme on the Ruvuma Asset until the deal completes, meaning we avoid the material dilution that would have been required in the event we retained our interest in the project.

The Board has no doubt whatsoever that this is wholly in the best interest of the Company and its shareholders. After an exhaustive sales process over the last couple years, it is evident that this is the best possible deal that we could achieve based on the macro backdrop and the investment required to further de-risk and commercialise our interest in Ruvuma. In Wentworth, we have found the perfect counterparty that can add value to the JV going forward, and their existing profile in Tanzania ensures lower deal execution risk and the best chance of a swift completion.

Upon completion, this deal enables the Board to focus on the execution of its stated strategy, with a significantly stronger balance sheet and cash that can be deployed right away to capitalise on the compelling opportunities that we have within the EAG JV’s deal pipeline. Those opportunities reflect our stated intention to create a cash generative, diversified business model which can grow through acquisition of and/or investment in sustainable energy assets. The divestment of Ruvuma simplifies our investment thesis and enhances our appeal to a broader universe of investors, including ESG investors who we believe will be attracted to our growth strategy.

We look forward to discussing the merits of this proposed transaction with our shareholders at the upcoming shareholder presentation, details on which are set out below.’

Katherine Roe, Chief Executive of Wentworth:

“This is a transformational transaction for Wentworth establishing us as a dual-asset, full-cycle E&P with a significantly enhanced resource base and production profile. The deal represents an attractively priced, low risk entry into a high growth opportunity which cements our position as a leading supplier of domestic gas to Tanzania.

“This compelling growth opportunity is fully aligned with our commitment to support the Government to reach its goal of providing universal energy access by 2030 in accordance with our purpose to empower people with energy and deliver value for Tanzania, Wentworth and all our stakeholders.”

The Ruvuma Asset

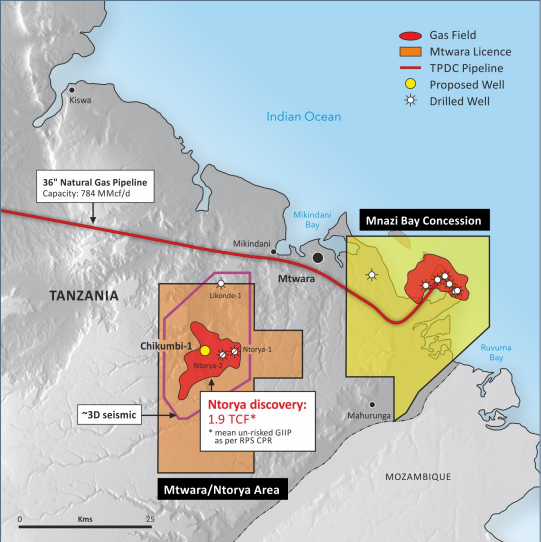

The Ruvuma asset contains the Ntorya-1 discovery well, drilled in 2012, and the Ntorya-2 appraisal well, drilled in 2017, and is estimated by RPS (2018) to have a mean estimated GIIP of c.1.9 Tscf. The Ntorya-1 gas discovery well is located approximately 30 km from the Madimba gas plant which is within the Mnazi Bay concession.

Development activity is progressing with a 338 km2 3D seismic survey currently underway before the drilling of the Chikumbi-1 appraisal well in late 2022 or early 2023. The Chikumbi-1 well aims to confirm 2C resources of 763 Bscf. The cost of the seismic survey and appraisal well net to Wentworth is estimated at $6.25 million.

Final Investment Decision (FID) is targeted for 2023 with first gas expected in late 2024 and an ultimate target production rate of up to 140 MMscf/d. The project will require construction of a pipeline from the gas field to the government operated Madimba gas facility, located approximately 30 km eastward, which is capable of handling 210 MMscf/d and is currently receiving most of the production volumes from the Mnazi Bay gas field. Gas from the Madimba gas facility will then be distributed via existing gas infrastructure to end users.

A commercialisation study performed by io oil and gas consultancy (a Joint venture between Baker Hughes and McDermott) in 2017 showed that a 140 MMscf/d Full Field development project would require approximately $143 million (gross) of capital expenditures. Actual costs and project scope will be dependent on a development plan agreed to by the Ruvuma JV partners and the government.

Details of the Transaction

The economic date of the Transaction is 1 January 2022.

The consideration structure ensures that the majority is only paid in a success case. The headline consideration of up to $16 million is payable in cash. Initial consideration of $3.0 million is payable in cash payable upon completion of the Proposed Transaction. Upon satisfaction of certain conditions Wentworth will make a loan of $0.5 million available to Scirocco (the “Initial Loan”). 50% of such Initial Loan is repayable in the event completion does not take place.

Deferred and contingent payments represent the remaining cash payment of $13 million which is due upon the following key milestones:

o $3.0 million on reaching FID;

o Up to $8 million through a minority share of net profit to Wentworth; and

o $2.0 million on reaching gross cumulative production of 50 Bscf.

Wentworth has agreed to a loan arrangement of up to $6.25 million with Scirocco to enable Scirocco to meet its cash call obligations and provide continuity to the work programme in the interim period to Completion. Any drawdowns under the Facility are subject to Scirocco shareholders’ approval and partner non pre-emption and the full amount of drawdowns (less $0.25 million of the Initial Loan) are repayable in the event of non-completion. The Facility will be secured by assignments of security by Scirocco in favour of Wentworth over the Licence Documents for the Ruvuma Asset. The grant of such security will be subject to the consent of the Minister for Energy in Tanzania and both parties will look to obtain such consent as soon as possible. The first $3.0 million to be drawn under the Facility is interest free, however, any amounts drawn in excess of $3.0 million will incur interest at a rate of 7% per annum until such time as the grant of the security in respect of the Facility is approved by the Minister for Energy in Tanzania.