East Africa to Witness Increased Upstream Activity in 2022

The three countries Kenya, Uganda and Tanzania could see investments of over $13 billion in the upstream sector from ongoing exploration and entry in the development stage. This is according to the Kenya and Tanzania Upstream outlooks unveiled free to the public earlier today on OilNews Africa website. The Uganda Tilenga EACOP Development stage outlook was also made public earlier the year

In particular, the huge chunk of this investment will be in the Kingfisher and Tilenga projects in Uganda and the East African crude Oil Pipeline EACOP in Uganda and Tanzania where over $10 billion has already been committed by partners Total Energies and CNOOC. The ongoing development works in Uganda is expected to have an event in especially the logistics industry with hundreds of tonnes of materials expected to have present huge opportunities for Kenya and Tanzania from where the goods will pass through.

In Kenya focus in the first half of 2022 will be on the Mlima-1 well being drilled by Eni-led joint venture of Qatar Energy and Total Energies estimated to cost $140 million. Results from the drilling are expected in the first quarter with the well expected to take 40 days to drill since spudding on 28th December 2021. Depending on the result there is expected to be follow-up wells that could further provide more detailed information on the geology and size of the resource should there be a discovery.

Later in the year there is the expected announcement from Tullow Oil, Africa Oil and Total Energies on reaching a final investment decision on the South Lokichar Development Area where expected capital expenditure is estimated at $3.4 billion according to the last revised design concept by Project Oil Kenya. the new plan involves producing oil from six oilfields with the well pads connected to the central processing unit (CPF) located in within a central hub the central facilities area near the Ngamia field via buried pipelines. Should FID be reached the construction will also involve the Lokichar to Lamu Crude Oil Pipeline (LLCOP) which will be an 890km heated oil pipeline from the oilfields in South Lokichar to the marine terminal in Lamu.

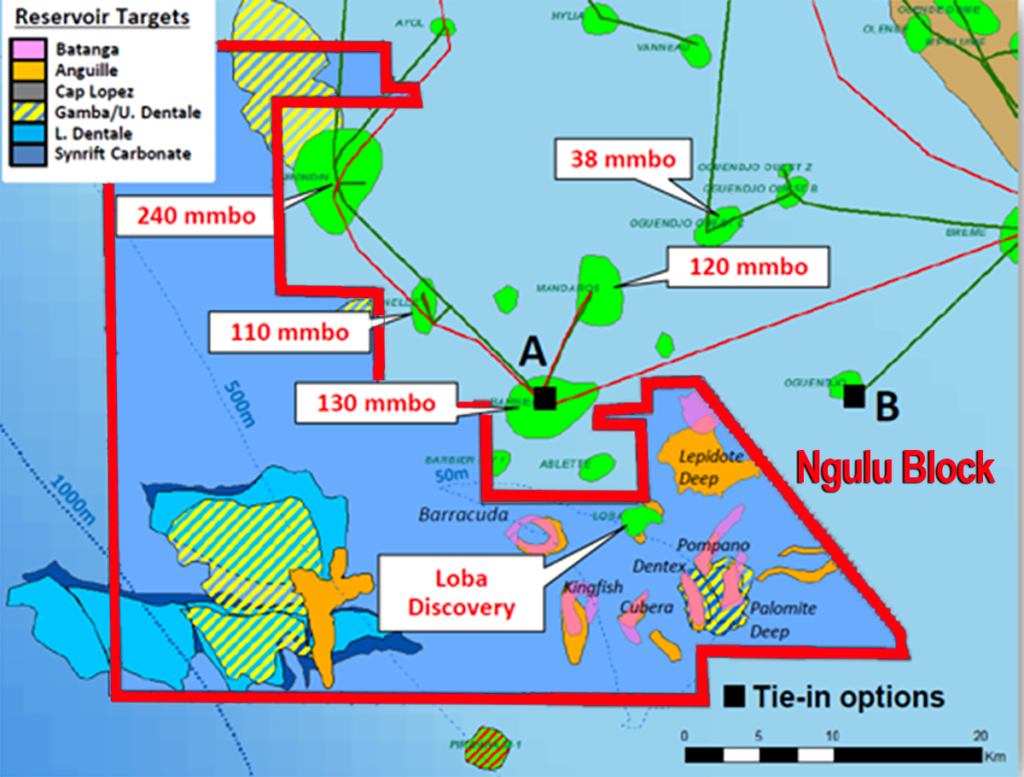

Elsewhere in the region work is picking up in the Ruvuma PSA where there is planned seismic and later drilling towards the end of the year. At the Kiliwani North license there are continuing remedial works to rehabilitate the KN1 well which has since ceased production while in Songo Songo commissioning of natural gas compressors within the Songas gas processing facility is ongoing. Worth watching will be negotiations with IOCs which hold offshore blocks with an estimated 57TCF of gas ready to development which could attract investment in excess of $20 billion.

Below are links to the three outlooks covering Kenya, Uganda and Tanzania:

KENYA: https://www.oilnewskenya.com/downloads/kenya-upstream-outlook-2022-2023/

TANZANIA: https://www.oilnewskenya.com/downloads/tanzania-upstrea…utlook-2022-2023/

UGANDA: https://www.oilnewskenya.com/down/