Tullow Oil Provides 2023 Operational Performance 2024 Outlook

Operational performance

In 2023, full year working interest production averaged 62.7 kboepd, including 6.9 kboepd of gas. Group working interest production is expected to increase year-on-year and our guidance range for 2024 is 62-68 kboepd, including c.7 kboepd of gas production.

| Group working interest production (kboepd) | FY 2023 | FY 2024 Guidance |

| Ghana oil | 42.6 | 48 |

| Jubilee oil | 32.5 | 39 |

| TEN oil | 10.1 | 9 |

| Non-operated portfolio oil | 13.2 | 11 |

| Gabon oil | 12.2 | 10 |

| Cote d’Ivoire oil | 1.0 | 1 |

| Gas production | 6.9 | 7 |

| Group | 62.7 | 62-68 |

Ghana

The start-up of production from the Jubilee South East project in July was a landmark event, marking a step change in the field’s production with average daily rates c.30% higher in the second half of the year compared to the first half with rates reaching levels over 100 kbopd.

Gross oil production from the Jubilee field averaged 83.4 kbopd (32.5 kbopd net) in 2023. This was below our expectations, primarily due to water injection reliability challenges and Jubilee South East starting up slightly later than planned. The water injection reliability issues were resolved in the fourth quarter of 2023, with upgraded capacity delivering record water injection rates and observable pressure response in the reservoirs, which will benefit 2024 production and beyond. Jubilee gas processing was also upgraded in 2023 and as a result, we have increased capacity to produce oil from wells with higher associated gas content. These important facility upgrades put us in a strong position to maintain production in the range of 90-110 kbopd towards the end of the decade.

Gross oil production from the TEN fields averaged 18.4 kbopd (net: 10.1 kbopd) during 2023, with improved pressure support from existing injection wells resulting inbetter management of decline. A planned shutdown was carried out in July and work was completed to improve asset integrity, enhance production through improved liquid recovery from gas and reduce flaring. Flaring from TEN reduced by over 50% post the shutdown, an important step forward in our target to eliminate routine flaring by 2025.

During the year, our operational performance continued to strengthen and average uptime across our Ghana FPSOs remained high at 96%. The drilling team also had excellent performance with seven wells (four Jubilee producers and three Jubilee water injectors) brought onstream during 2023. The cost of drilling wells in 2023 was on average around 20% lower and c.38 days faster than the previous campaign in 2018-2020, achieving top-quartile industry performance. These cost savings and efficiencies have been driven by reducing non-productive time, improved well design and more effective contracting.

Five new Jubilee wells (three producers and two water injectors) are scheduled to come onstream in 2024. The first water injector was brought on stream in January, and two producers were brought on stream in February, with gross production currently averaging over 100 kbopd. We expect to complete the current drilling programme around the middle of the year, approximately six months ahead of schedule. We then intend to take a drilling break in Ghana with plans to resume drilling in 2025. During this time, we will optimise our plans for the next phase of investment in Ghana while the existing well stock and upgraded water injection capacity sustains production at Jubilee and TEN decline continues to be effectively minimised through improved pressure support.

Net gas production in Ghana averaged 6.4 kboepd in 2023 and marked the first commercialisation of associated gas from the Jubilee field. The interim Gas Sales Agreement, initially valued at $0.50/mmbtu, was amended in July 2023 to a price of $2.90/mmbtu and subsequently increased in November to $2.95/mmbtu, after applying year-on-year inflation indexation. This agreement represents a revenue stream for Tullow of c.$4 million per month.

During the year, discussions continued with the Government of Ghana on the amended TEN Plan of Development (PoD) and the long-term gas sales agreement. We remain committed to reaching agreement and progressing a number of identified projects at TEN in addition to commercialising the material gas resource base.

In February 2023, we announced that Tullow Ghana Limited (TGL) had filed requests for arbitration with the International Chamber of Commerce in London in respect of two disputed tax assessments received from the Ghana Revenue Authority (GRA). The assessments relate to the disallowance of loan interest deductions for the fiscal years 2010 – 2020 and proceeds received by Tullow Oil plc during the financial years 2016 to 2019 under the Group’s corporate Business Interruption Insurance policy.

Tullow had also previously filed a request for arbitration in respect of a separate assessment for Branch Profits Remittance Tax of $320 million in 2021. A hearing in respect of this dispute took place in October 2023 with an outcome expected this year.

We believe that resolution through international arbitration will bring certainty, which is in the best interest of all stakeholders. In the meantime, we continue to engage with the Government of Ghana, including the GRA, with the aim of resolving these disputes on a mutually acceptable basis.

Non-operated and exploration portfolios

In line with expectations, production from our non-operated portfolio in Gabon and Côte d’Ivoire averaged 13.7 kboepd net in 2023 (2022: 16.7 kboepd net), including 0.5 kboepd of gas production in Côte d’Ivoire.

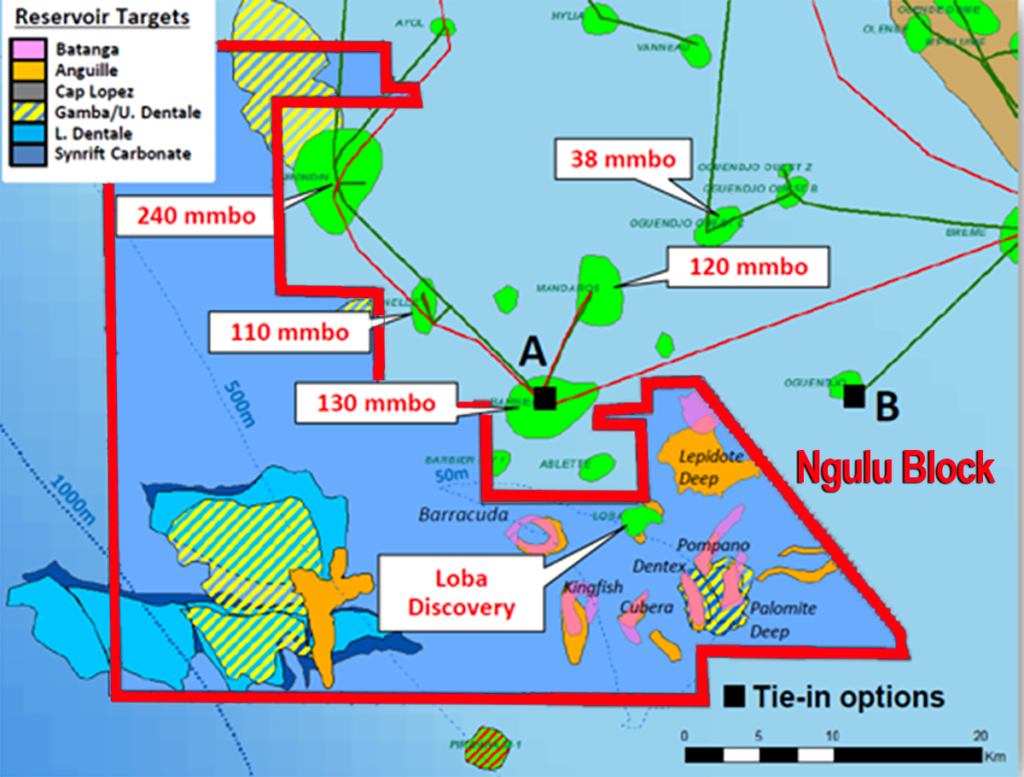

Gabon is a key part of our production and infrastructure-led exploration (ILX) portfolio and in 2023 we took actions that place the Tchatamba facilities as a core hub for Tullow. In April, we announced the cashless asset swap agreed with Perenco that enabled us to take more material positions in key fields around Tchatamba. In August, the Government of Gabon approved the extension of several of our licences to 2046, reflecting the future potential of the fields and the longevity of the Tchatamba facilities. 2P reserves additions from the licence extensions and the asset swap amounts to c.6 mmbbls with a further c.3 mmbbls 2P positive reserves revision from asset performance, overall representing c.190% reserves replacement in 2023. During 2024, operations in Gabon will focus on infill drilling to sustain production or minimise decline across the licences, as well as two ILX wells at the Simba licence.

On Espoir in Côte d’Ivoire, we continue to work with the operator to establish the best way forward for the asset. On exploration licences CI-524 and CI-803, we are maturing the prospect inventory ahead of drill candidate selection for an exploration well to potentially be drilled in 2025.

Kenya

Kenya remains a material option to drive value and growth for Tullow. An updated Field Development Plan (FDP) which intends to develop 470 mmboe of 2C resources to produce up to 120 kbopd, was submitted to the Government in March 2023. We have since worked collaboratively with the Government as they evaluate the FDP. Once their evaluation is concluded, the FDP will be submitted to the Cabinet Secretary for Energy and Petroleum for review before submission to Parliament for final approval. The development has been designed to be robust at lower oil prices and we continue discussions with prospective strategic partners for this project.

In June 2023, our interest in Kenya increased from 50% to 100% as a result of the withdrawal of our Joint Venture Partners for differing reasons. The increased interest provides us with greater strategic flexibility. While we continue to progress the FDP, we are also actively working with the Government of Kenya in developing options to accelerate production and cash flow to unlock value from this well-matured resource base.

Reserves and resources

At the end of 2023, audited 2P reserves were 212 mmboe (2022: 229 mmboe). During the year, 23 mmboe of 2P reserves were produced with a replacement ratio of 26%. Additions were primarily from the extension of production licences in Gabon and the maturation of several infill wells, both in Gabon and the Jubilee area. These additions were partly offset by reductions in TEN 2P reserves, mainly driven by a reduced near-term development programme in light of the ongoing delays to gain Government approval for the TEN amended PoD. Around 30 mmboe of net gas resources remain classified as 2C pending the approval of the TEN amended PoD and Gas Sales Agreement. Commercialisation of these gas resources would place TEN on a much firmer economic footing and support the maturation of several identified projects.

Tullow’s asset base continues to have significant value, and as of 31 December 2023, Tullow’s audited 2P NPV10 was $3,406 million. This is slightly down from 2022 ($3,895 million), driven largely by TEN revisions and a lower long-term oil price assumption as defined by independent third-party reserves auditor, TRACS.

The Group’s audited 2C resources increased to 745 mmboe at the end of 2023 (2022: 605mmboe), reflecting the material scale of opportunity Tullow has to convert resources into reserves to sustain long-term production. As we now hold 100% of our Kenya licences, net contingent resources have doubled to 470mmboe. 54mmboe of contingent resources has also been removed following the sale and exit from Guyana.

Outlook

After reaching an important inflection point in our business plan in 2023, Tullow has a strong and unique foundation to create material value for our investors, host nations and wider stakeholders and we look to the future with confidence.

We will continue to run our business with the same rigorous financial discipline, prioritising the highest returns and focusing on value-accretive investments. Our balance sheet will continue to strengthen as we further reduce our debt and optimise our capital structure. We have made good progress toward delivering our target of $800 million of free cash flow between 2023 and 2025 and given the quality of our resource base, the opportunity set ahead of us and a reducing cost outlook, we expect to maintain these levels of free cash flow generation in subsequent years.

With a strong balance sheet and this sustainable free cash flow outlook, our business will be well placed to deliver value to our shareholders through organic and inorganic growth and capital returns.